My trick to making money in the market is finding a business that is misunderstood and therefore valued by the market incorrectly. I believe I have done that with $ACTC(merging with Proterra):Proterra is an EV-bus, energy solutions, and electric battery maker. Made completely in the USA (California+South Carolina) I am not a financial advisor.

First off valuation–

Proterra’s merger is valued at 1.6b enterprise value and they have 852m cash on hand. So at 25 the pro format valuation is around 6b after merger. In addition, Chamath Palihapitiya is leading the 415 million dollar PIPE.

But don’t think this valuation is expensive at 25 and here’s why. The market is pricing Proterra as an EV bus company. When in reality it is more of a battery company.

Now for the DD:

Management-

I firmly believe management is the most important aspect of any young company.

-First off, this is not comparable to any other younger stage EV company when it comes to management. The most impressive of all, is that Proterra has many execs with experience at Tesla including the Chief Technology Officer, Chief Operating Officer, and Co-founder. But most importantly, the Energy Secretary that Biden nominated is Director Jennifer Granholm. She is a board member at Proterra!

In addition, the ArcLight team includes two directors on the Clean Energy for Biden team

Now on to the financials:

-Proterra received 193m in revenue last year(during the pandemic)

-Their projected revenue for the coming years based on backlog(based on 750m+ backlog for buses)

Conservative and based on CURRENT backlog:

Revenue Growth/Gross Margin compared to other Publicly Traded Companies

More Information about financials:

My only concern is the Gross Profit, but I believe that will improve overtime

Now that we got that out of the way we can get into the fun stuff. I’m going to break this up into 3 parts, electric busses, electric solutions, and what I believe to be most impressive, their battery solutions/partnerships.

Electric buses:

Proterra Transit

-Currently this is their main source of revenue

-Over 130 customers in 43 states so far!

-Some of the most notable being the National Park Service, colleges such as of this week Harvard, Duke(go blue devils!), and Georgia. Also, Jill, and airports such as SFO and JFK.

To see the full list:https://www.proterra.com/company/our-customers/

This map shows the location of their customers:

As of right now they have:

And yes you read that right, over 50 percent electric transit bus market share.

![]()

-Proterra is also breaking boundaries in the pricing of their buses. They offer an option to pay the battery off overtime like gasoline. This gives particularly transit departments a better way to fit it into their budget.

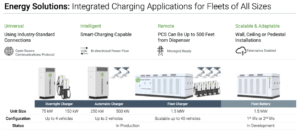

Electric Solutions:

-In addition to their busses Proterra also provides charging stations.

Here is how their charging stations work:

Customers are incentivized to buy these charging station because of Proterra’s Cloud-based data-system, Apex Software. This helps gives users a centralized singular area to check the overall statistics of their fleet.

-Proterra has installed over 50 Megawatts of these charging stations nationwide.

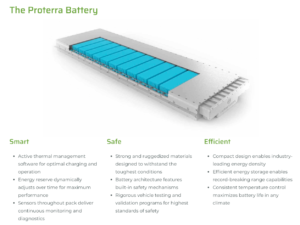

Batteries/Partnerships:

Proterra currently has some of the best batteries in the game. Their batteries have 330 miles for their buses, and can be used across a number of applications. This is what I think their insane growth in the future will come from.

Their partnerships with batteries(Proterra Powered) include:

-Daimler’s Thomas Built Buses. Daimler has 50 percent market share in the school bus market. Daimler worth 85b! Not only are they working with Proterra, but have a 200m investment in them. This gives Proterra access into this market and an advantage over competitors like Lion Electric($NGA)

-Komatsu(worth 23b) for their electric excavator. This gives Proterra access to another completely different market and makes them now competitors with the 107b CAT.

-Electric Last Mile Solutions. Going public through FIII. Company worth 1.8b, and this helps Proterra gain traction in the massive delivery van market.

-Vanhool, for their coach bus. They have an estimated 2b in annual revenue. Legitimizing Proterra in the electric luxury bus market as well.

–Bustech for busses for the Australian climate. Overall, bettering their buses.

– Freightliner Custom Chassis Corporation (FCCC) to develop the MT50e, a new all-electric delivery truck chassis. This gives Proterra another access to revenue.

Conclusion:

This company has so much going for it, they should be worth at least 15b($70). Market doesn’t understand the potential of all these battery partnerships. This is a great opportunity to take advantage of. Good luck to all!

Sources:

https://www.proterra.com/wp-content/uploads/2021/01/ACTC-Proterra-Investor-Presentation.pdf

Disclaimer: The stocks mentioned in my newsletter and blog are not intended to be a list of buy recommendations but rather some ideas for your watchlist. Perhaps they end up in your own portfolio after you conduct your own research and due diligence. Some of the stocks mentioned in my newsletters have smaller market capitalizations and therefore can be more volatile. I always encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizing in accordance with your own risk tolerance and investment objectives.

{kind=link}